- Author: Windsor Life Settlements

- Published Date:

Chapter 2: Do I Need to Be Licensed or Certified to Buy Policies?

For investors considering an allocation to life settlements, one of the first and most common questions is: Do I need to be licensed to participate? The answer depends on how you intend to invest — and whether you’re purchasing policies directly or investing through a fund structure.

This chapter explains the legal and regulatory environment surrounding life settlements, the role of licensing, and what both individual and institutional investors need to know before entering the market.

Life Settlements Are Regulated at the State Level

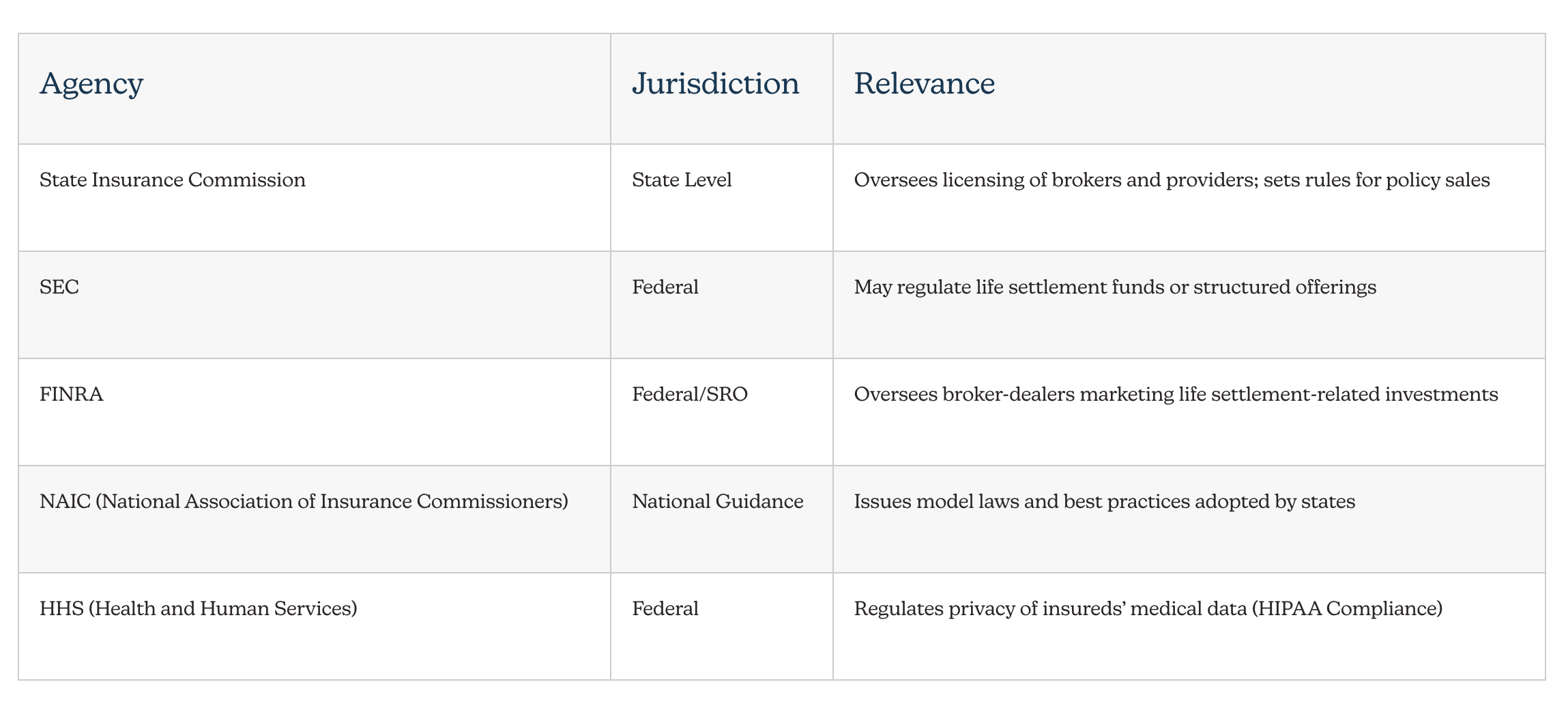

Unlike securities or investment funds, life settlements are primarily governed by state insurance laws — not federal securities law. As of today, 43 U.S. states (plus Puerto Rico) regulate life settlement transactions, representing over 90% of the U.S. population. Each state has its own laws defining licensing requirements, investor eligibility, disclosure standards, and permissible transactions.

This state-by-state approach creates a patchwork of compliance — which is one reason why investors typically engage through licensed providers or brokers who specialize in navigating these variations.

📌 Key Note: While the transaction of selling a policy is regulated at the state level, certain fund structures and investment vehicles associated with life settlements may also fall under federal jurisdiction (SEC, FINRA).

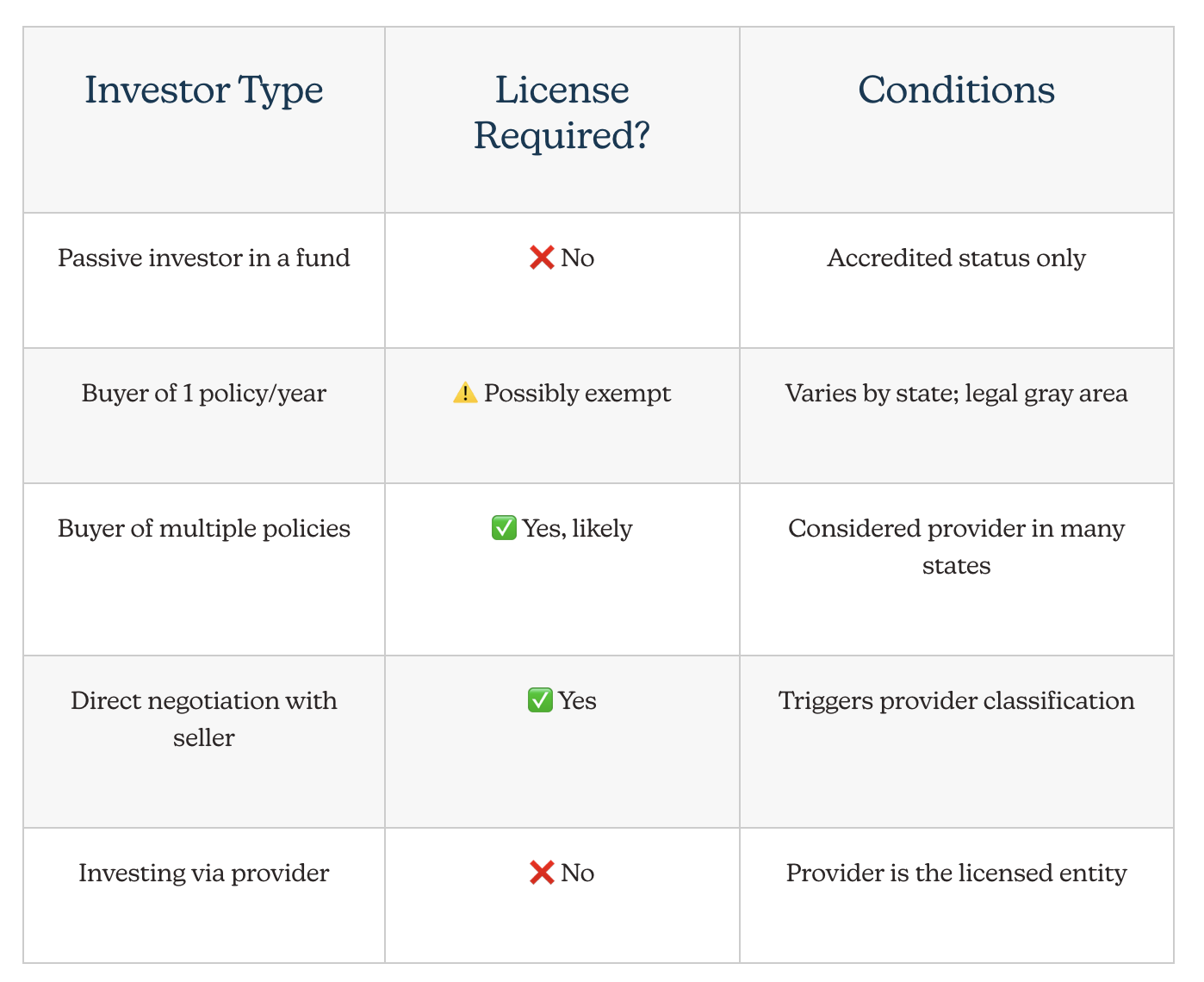

Do Investors Need to Be Licensed to Invest?

You typically do not need to be licensed if you are:

📌 This is the route taken by the vast majority of individual and institutional life settlement investors. |

When You May Need a License:In some states, if you act as the direct buyer of a policy from a consumer, and especially if you do this repeatedly, you may be considered a life settlement provider under state insurance laws — which requires a license. States such as New York, California, Florida, and Texas require providers to:

|

|

The “One-Policy Rule” Some states allow an individual to purchase one policy per year without being classified as a provider, but that exemption may apply only to consumers and not professional investors. Legal interpretations vary and are not always clearly published. Source: NAIC Viatical Settlements Model Act §3, and various state insurance codes (e.g., California Insurance Code §10113.1, New York Insurance Law §7810) |

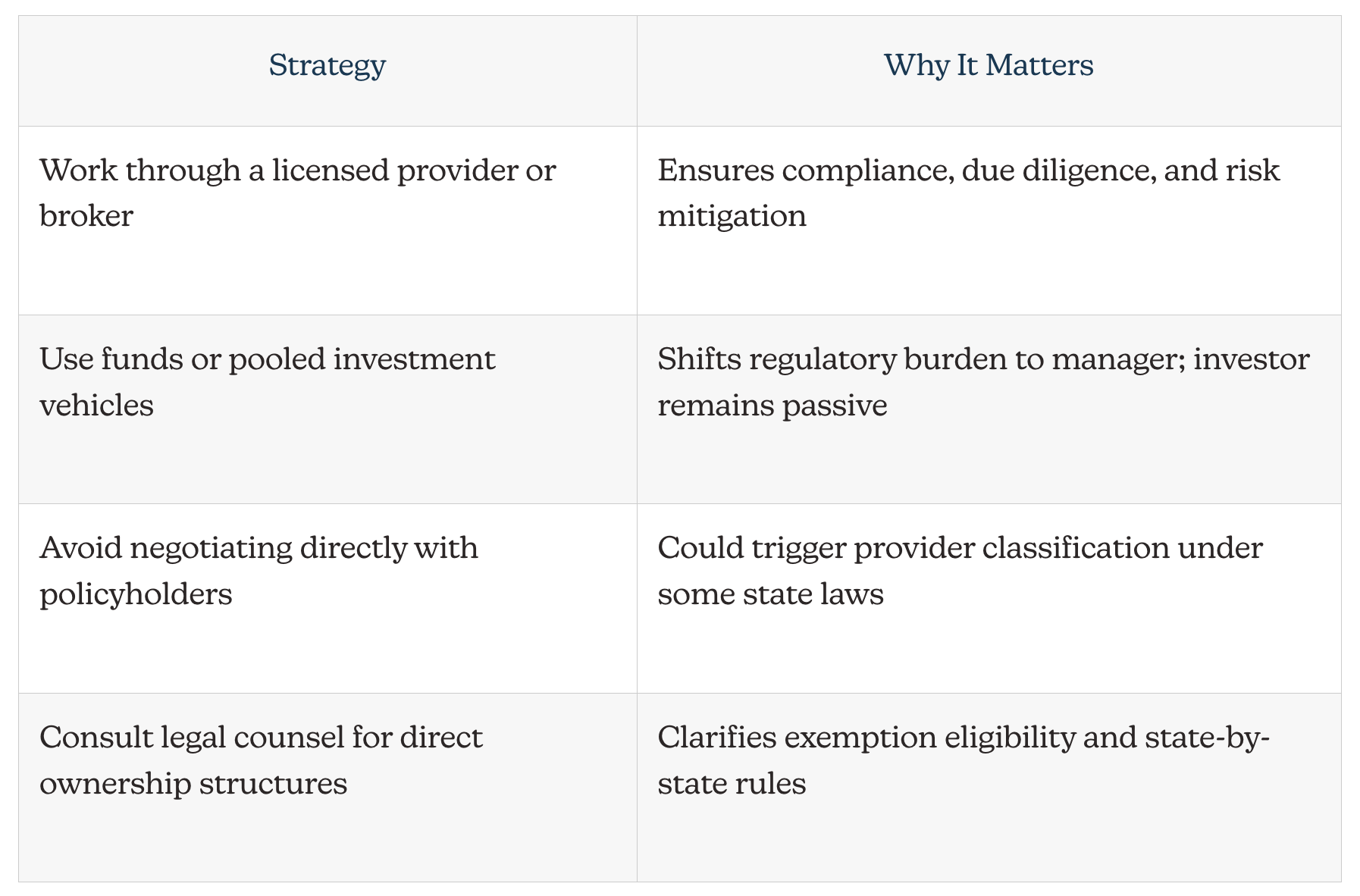

Best Practices for Investors

Licensing Summary

The Role of Providers and Brokers in Compliance

Life settlement providers and brokers are licensed professionals who serve as intermediaries between policy sellers and investors. They are responsible for ensuring regulatory compliance in every transaction, including:

- Verifying policy eligibility and insurable interest laws

- Conducting anti-fraud and identity checks

- Handling disclosures and documentation

- Managing transfer and beneficiary designations

- Ensuring privacy protections (e.g., HIPAA compliance)

Providers are often the regulated entity through which investors gain access to policies, helping insulate the investor from legal risk and state-specific licensing burdens.

Legal Considerations and Best Practices for Investors

Even though investors may not need to be licensed, they must approach the asset class with care. Some key legal best practices include:

- Work with licensed providers or brokers only — verify their licenses via state insurance commission databases

- Use third-party custodians or trustees to hold policy interests when possible

- Avoid directly negotiating with policyholders unless legally authorized

- Review contracts thoroughly, including rights, obligations, and disclosures

- Ensure data privacy compliance when handling insured health information (e.g., HIPAA, GLBA)

It is also wise to consult legal counsel experienced in life settlements — especially when purchasing policies directly or co-investing with others in a fund structure.

Overview of Key Regulatory Bodies

While life settlements are primarily state-regulated, several key regulatory bodies may become relevant depending on how investment structures are designed.

Conclusion: Clarity Through Professional Intermediaries

While life settlement transactions are governed by a complex patchwork of regulations, the good news is that most investors do not need to be licensed or certified — as long as they invest through reputable, regulated intermediaries.

Windsor Life Settlements works exclusively with licensed brokers and providers to ensure every transaction is fully compliant with state and federal guidelines. Our role is to streamline the process, shield investors from regulatory complexity, and provide access to rigorously underwritten policy assets.

By working with established partners and adhering to industry best practices, investors can participate in this unique asset class with confidence, clarity, and compliance. Windsor Life Settlements works exclusively through licensed providers and ensures full regulatory adherence on all investor-facing transactions.

- Author: Windsor Life Settlements

- Published Date:

Windsor Life Settlements

Questions? Comments?

We’re available by phone Monday-Friday 9am-5pm CT