Most people don’t qualify, despite what the commercials might suggest. Life settlements are typically for policyholders over age 75 or those with serious health conditions.

Most people don’t qualify, despite what the commercials might suggest. Life settlements are typically for policyholders over age 75 or those with serious health conditions.

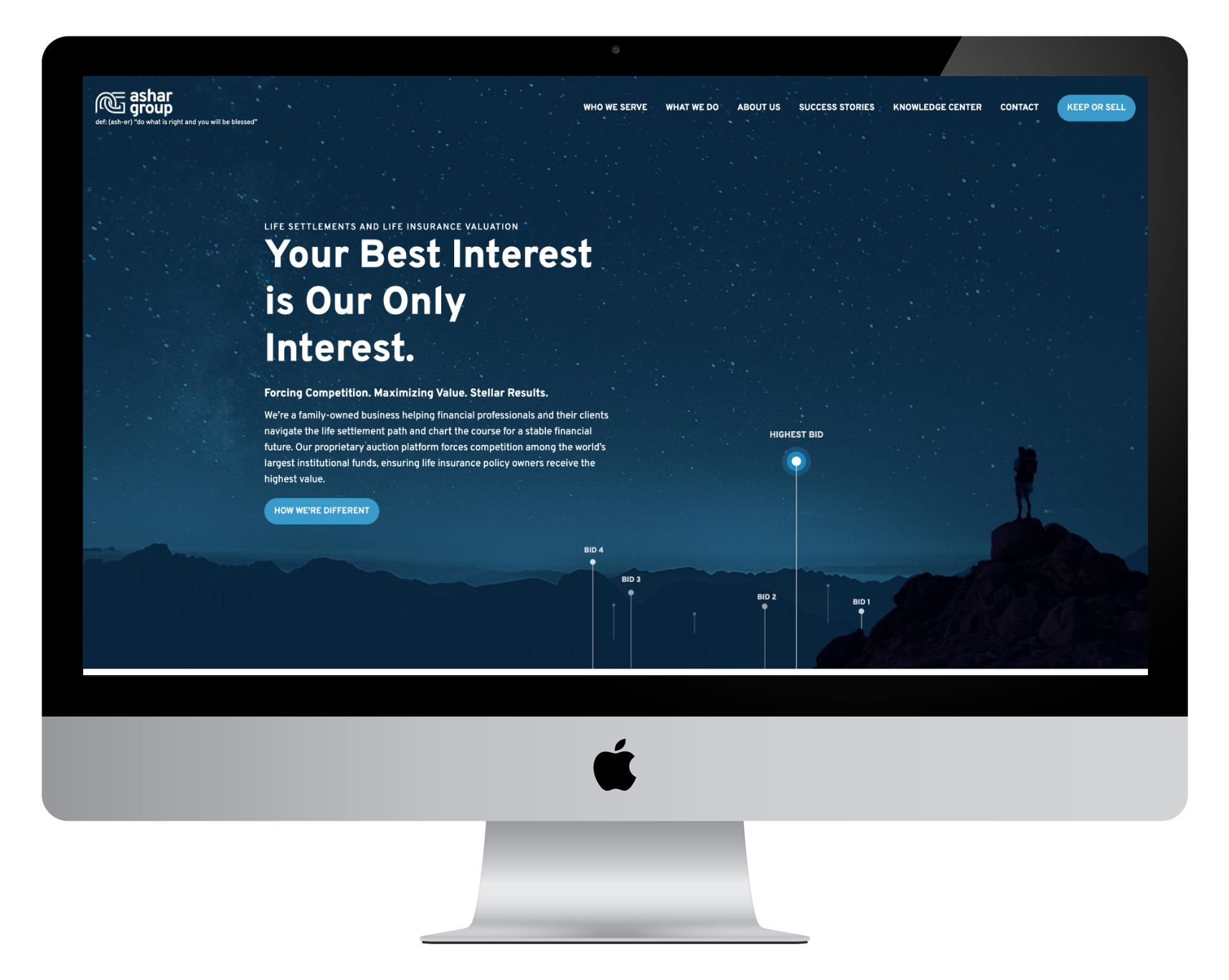

Three policies, three carriers, three sizes. A $250,000 policy, a $1,500,000 policy and a $7,000,000 policy, each taken to the full market of institutional buyers....

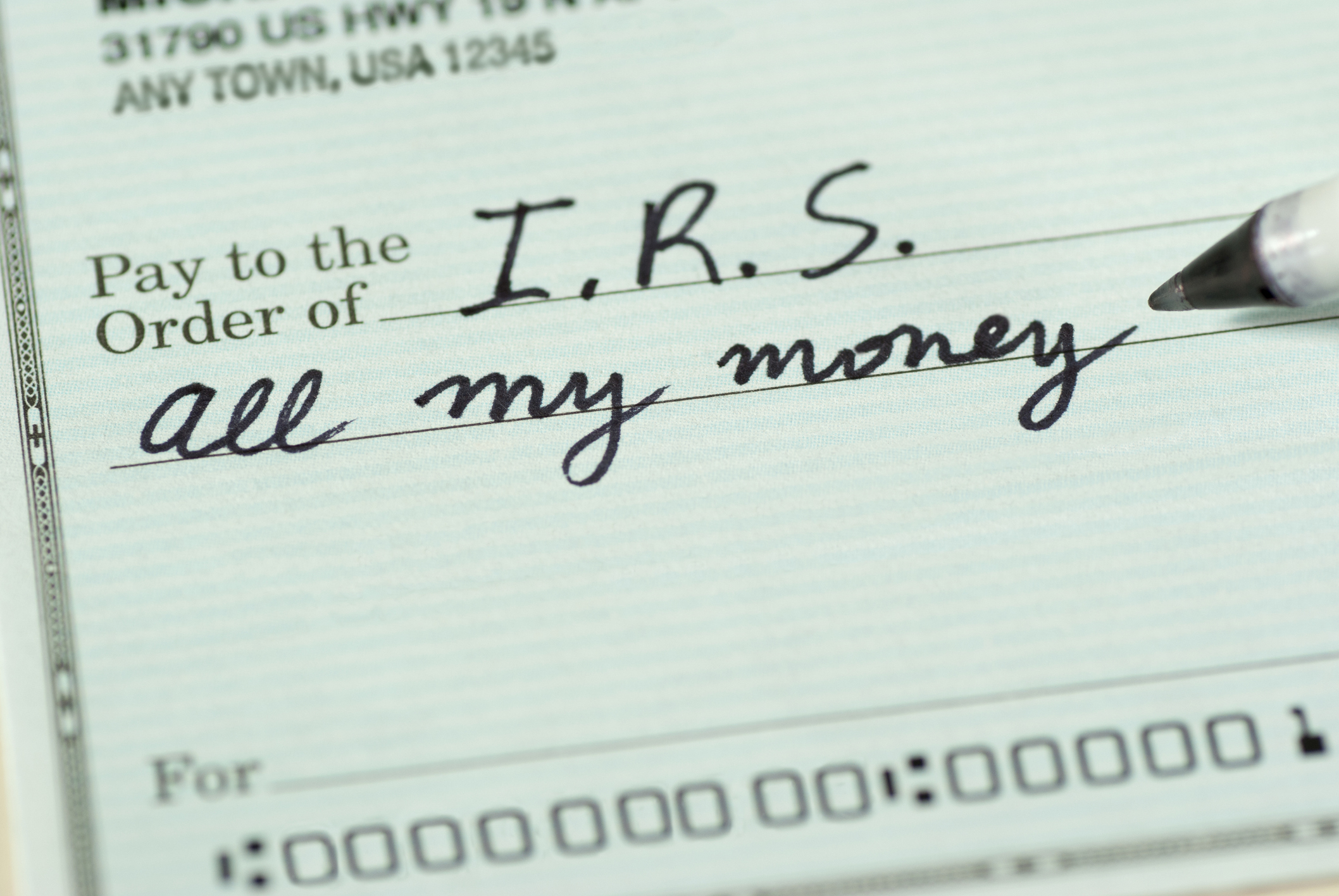

Life settlements are taxed more favorably than sellers fear. Part of the proceeds is usually a tax-free return of premiums.