- Author: Windsor Life Settlements

- Published Date:

Chapter 3: The Investment Case for Life Settlements

In an environment of rising interest rate uncertainty, equity market volatility, and compressed yields across traditional fixed-income products, investors are under pressure to find stable, risk-adjusted returns. Life settlements offer a unique alternative — one that delivers consistent performance, minimal market correlation, and long-term predictability.

This chapter outlines why more institutions and accredited investors are adding life settlements to their portfolios — and why this asset class deserves consideration alongside real estate, private equity, and bonds.

Non-Correlation to Stock and Bond Markets

One of the most compelling reasons to invest in life settlements is their independence from market volatility. Unlike stocks, bonds, or even real estate, life settlements are not influenced by interest rates, inflation, GDP growth, or geopolitical events. Instead, their returns are based on a single, actuarially-modeled event: the passing of the insured individual.

Because life settlement performance is not tied to economic cycles, investors can use this asset class as a natural diversifier — a source of returns when traditional markets are under stress. This low correlation has made life settlements increasingly attractive to institutions seeking downside protection during bear markets or stagflationary environments.

Key Stat: According to industry data, the correlation coefficient between life settlements and the S&P 500 has been estimated at near zero (0.05), underscoring its true independence from equity market swings.

Predictable Cash Flows and Defined Timelines

Life settlements offer high visibility into future outcomes. Once a policy is purchased, the investor knows:

- The face value of the policy (death benefit)

- The premium obligations required to keep it active

- The actuarially-estimated life expectancy of the insured

This allows for modeling of returns across short, medium, and long-term holding periods. In properly structured portfolios, cash flows can be projected with a surprising degree of accuracy — especially when policies are diversified across age ranges, health conditions, and carriers.

Most investors target net internal rates of return (IRRs) between 8% and 12%, depending on leverage, fees, and life expectancy assumptions. Once a policy matures, the investor receives the death benefit — a known payout tied to a life event, not a market outcome.

Portfolio Diversification Benefits

Institutional investors understand that asset allocation is the foundation of risk-adjusted performance. Life settlements offer portfolio construction benefits by:

- Reducing volatility: Because their value doesn’t fluctuate daily like equities or real estate

- Enhancing Sharpe ratios: Due to relatively high, consistent returns with low standard deviation

- Providing a time-based counterbalance: Unlike most investments, life settlements increase in value the longer they are held (closer to maturity)

A typical life settlement fund may include hundreds of policies across dozens of carriers, further spreading risk and creating a bond-like laddering effect where maturities occur over time. This makes them suitable for income-oriented strategies, capital preservation, and pension-style mandates.

Historical Performance and Market Maturation

The life settlement market has evolved substantially over the past 20 years. Once a fragmented and opaque sector, it is now regulated in over 43 U.S. states, with increasing institutional participation and third-party servicing firms that manage policy tracking, premium payments, and insured monitoring.

📈 Historical Benchmarks:

- Between 2004 and 2019, life settlement funds tracked by industry data providers returned net annualized returns between 8% and 12%.

- In 2022, amid global market turmoil, several funds in the space reported positive single-digit returns, while the S&P 500 declined over 18%.

- Some well-managed portfolios report Sharpe ratios exceeding 1.5, placing them in line with strong hedge fund performance, but without leverage or market exposure.

Institutional capital — from Blackstone, Apollo, and other large managers — has poured into the space, validating the model and increasing transparency. As data improves and secondary market infrastructure matures, performance consistency is expected to further improve.

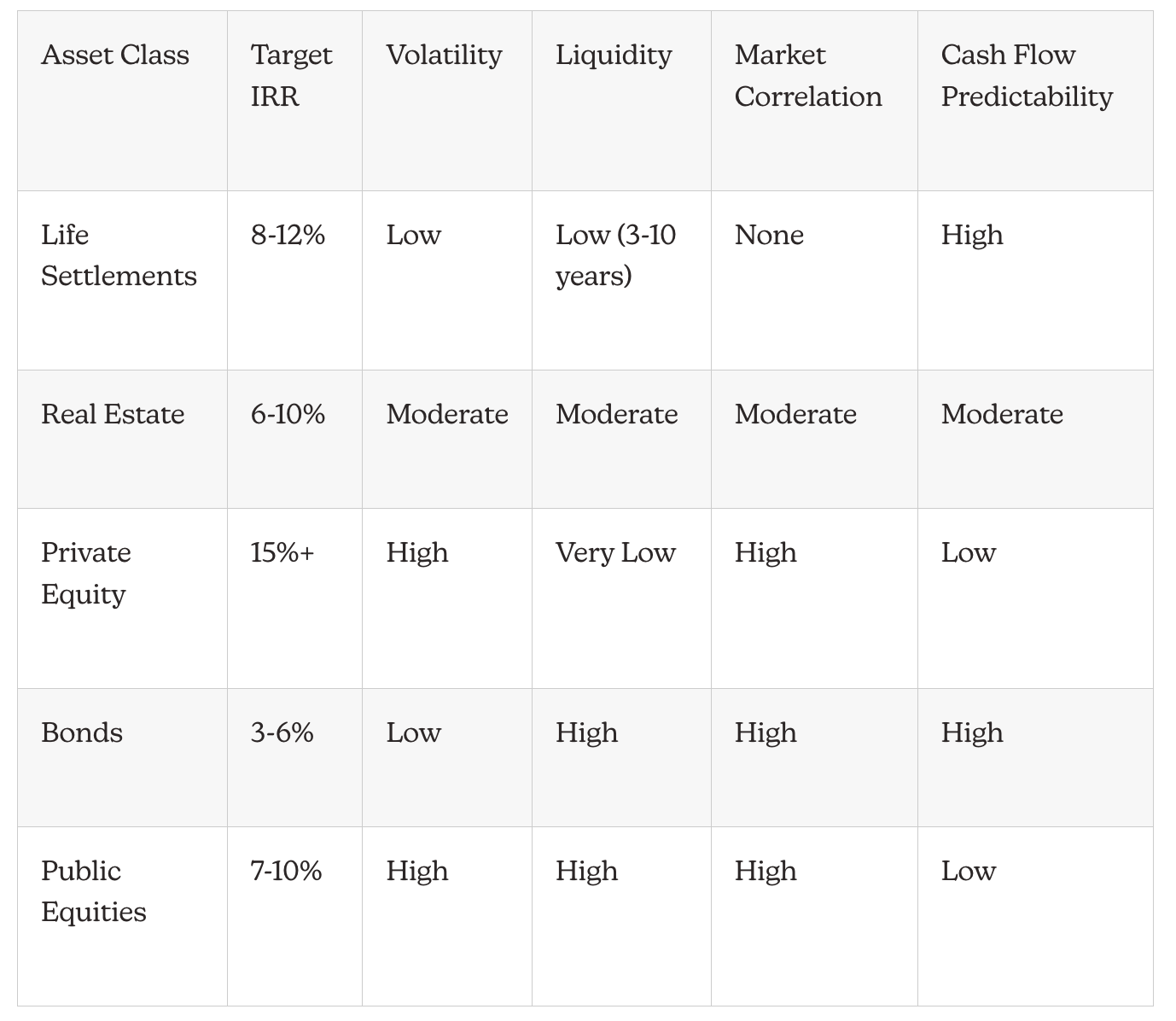

Comparison to Other Alternatives

To truly understand the appeal of life settlements, it helps to compare them to more traditional alternatives:

Life settlements occupy a rare space on this chart: high returns with low volatility and zero correlation — attributes highly sought after in institutional portfolio design.

Conclusion: A Strategic Allocation Opportunity

For investors seeking to hedge against economic shocks, generate consistent income, and build portfolios that aren’t dependent on the performance of public markets, life settlements offer a data-driven, actuarially-backed alternative.

The opportunity is not just in yield — it’s in control and clarity. With defined maturities, known costs, and independent timelines, life settlements allow investors to sidestep the noise of the market and build wealth from an overlooked corner of the financial system.

In the next chapter, we’ll explore the risks — including longevity and liquidity — and how experienced managers mitigate them across diversified portfolios.

- Author: Windsor Life Settlements

- Published Date:

Windsor Life Settlements

Questions? Comments?

We’re available by phone Monday-Friday 9am-5pm CT